Insights Ahead: Polaris's Quarterly Earnings

Polaris (NYSE:PII) is preparing to release its quarterly earnings on Tuesday, 2025-07-29. Here's a brief overview of what investors should keep in mind before the announcement.

Analysts expect Polaris to report an earnings per share (EPS) of $0.01.

Polaris bulls will hope to hear the company announce they've not only beaten that estimate, but also to provide positive guidance, or forecasted growth, for the next quarter.

New investors should note that it is sometimes not an earnings beat or miss that most affects the price of a stock, but the guidance (or forecast).

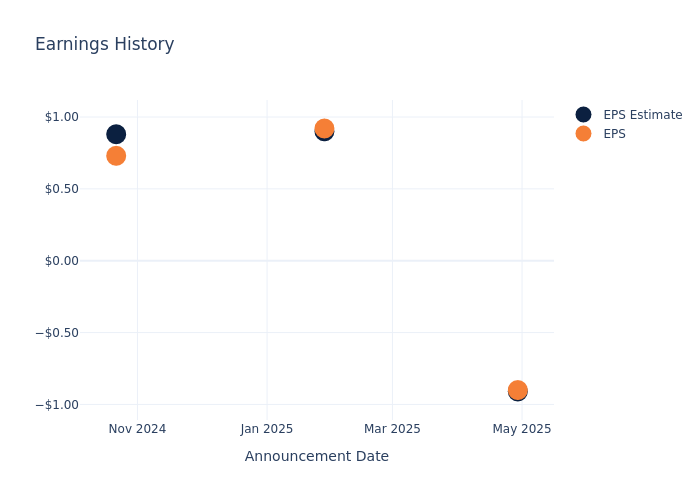

Performance in Previous Earnings

In the previous earnings release, the company beat EPS by $0.01, leading to a 0.38% increase in the share price the following trading session.

Here's a look at Polaris's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | -0.91 | 0.90 | 0.88 | 2.23 |

| EPS Actual | -0.90 | 0.92 | 0.73 | 1.38 |

| Price Change % | 0.0% | -5.0% | -4.0% | -7.000000000000001% |

Stock Performance

Shares of Polaris were trading at $50.24 as of July 25. Over the last 52-week period, shares are down 40.62%. Given that these returns are generally negative, long-term shareholders are likely bearish going into this earnings release.

Analysts' Perspectives on Polaris

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Polaris.

The consensus rating for Polaris is Neutral, based on 7 analyst ratings. With an average one-year price target of $35.43, there's a potential 29.48% downside.

Peer Ratings Comparison

The below comparison of the analyst ratings and average 1-year price targets of YETI Holdings, Topgolf Callaway Brands and Brunswick, three prominent players in the industry, gives insights for their relative performance expectations and market positioning.

- Analysts currently favor an Outperform trajectory for YETI Holdings, with an average 1-year price target of $39.43, suggesting a potential 21.52% downside.

- Analysts currently favor an Neutral trajectory for Topgolf Callaway Brands, with an average 1-year price target of $7.0, suggesting a potential 86.07% downside.

- Analysts currently favor an Buy trajectory for Brunswick, with an average 1-year price target of $65.33, suggesting a potential 30.04% upside.

Key Findings: Peer Analysis Summary

The peer analysis summary presents essential metrics for YETI Holdings, Topgolf Callaway Brands and Brunswick, unveiling their respective standings within the industry and providing valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Polaris | Neutral | -11.55% | $245M | -5.31% |

| YETI Holdings | Outperform | 2.85% | $201.72M | 2.21% |

| Topgolf Callaway Brands | Neutral | -4.54% | $667.50M | 0.09% |

| Brunswick | Buy | 18.43% | $303.90M | 3.14% |

Key Takeaway:

Polaris ranks at the bottom for Revenue Growth and Gross Profit, with negative growth and profit margin. It also has the lowest Return on Equity among its peers. Overall, Polaris is positioned unfavorably compared to its peers in terms of financial performance metrics.

Unveiling the Story Behind Polaris

Polaris designs and manufactures off-road vehicles, including all-terrain vehicles and side-by-side vehicles for recreational and utility purposes, snowmobiles, and on-road vehicles, including motorcycles, along with the related replacement parts, garments, and accessories. The firm entered the marine market after acquiring Boat Holdings in 2018, offering exposure to another segment of the outdoor lifestyle market. Polaris products are retailed through more than 2,500 dealers in North America and 1,500 international dealers as well as more than 25 subsidiaries and 90 distributors in more than 100 countries outside North America.

Understanding the Numbers: Polaris's Finances

Market Capitalization: Exceeding industry standards, the company's market capitalization places it above industry average in size relative to peers. This emphasizes its significant scale and robust market position.

Decline in Revenue: Over the 3 months period, Polaris faced challenges, resulting in a decline of approximately -11.55% in revenue growth as of 31 March, 2025. This signifies a reduction in the company's top-line earnings. As compared to its peers, the revenue growth lags behind its industry peers. The company achieved a growth rate lower than the average among peers in Consumer Discretionary sector.

Net Margin: The company's net margin is a standout performer, exceeding industry averages. With an impressive net margin of -4.35%, the company showcases strong profitability and effective cost control.

Return on Equity (ROE): Polaris's financial strength is reflected in its exceptional ROE, which exceeds industry averages. With a remarkable ROE of -5.31%, the company showcases efficient use of equity capital and strong financial health.

Return on Assets (ROA): The company's ROA is a standout performer, exceeding industry averages. With an impressive ROA of -1.22%, the company showcases effective utilization of assets.

Debt Management: The company faces challenges in debt management with a debt-to-equity ratio higher than the industry average. With a ratio of 1.78, caution is advised due to increased financial risk.

To track all earnings releases for Polaris visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.