These Mall Landlords Just Hit Jolly 52-Week Highs

It appears that Christmas has come a bit early for investors who own shares of mall landlords Simon Property Group Inc (NYSE: SPG), General Growth Properties Inc (NYSE: GGP) and Macerich Co (NYSE: MAC).

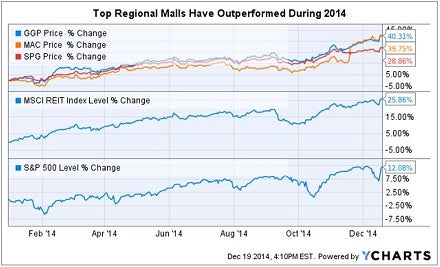

At the end of trading on Friday, December 19, 2014 -- the last full week prior to the Christmas holiday -- all three of these equity REITs focused on owning and operating Class-A malls hit 52-week highs.

A Strong Week

During intra-day trading on December 19, General Growth hit $28.42, Macerich reached $83.28 and Simon topped out at $185.95, prior to pulling back slightly at the end of the day.

A Very Strong Year

In a year that has seen equity REITs that own portfolios of commercial real estate outperform the broader market by over 100 percent to date, despite the naysayers, these three Class-A mall operators have performed even better.

Other Side Of The Coin

It appears that a steadily improving U.S. economy, drastically lower gas prices and more sophisticated omnichannel offerings by mall retailers have all combined to create a very happy holiday season for investors in Class-A malls that typically generate $600 per square foot of sales, or more. However, it has been a different story for the former Simon malls and open-air centers that have much lower sales per square foot.

A Diamond In The Rough?

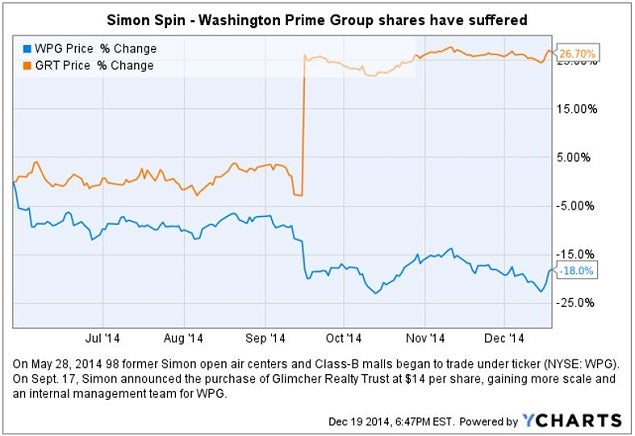

On May 28, Simon consummated a spin-out previously announced back in December 2013 separating the ownership and operations of its malls with lower sales per square foot, and its open-air centers into Washington Prime Group Inc (NYSE: WPG).

The 44 enclosed Simon malls that were transferred to Washington Prime Group had average sales of only $300 per square foot.

Simon chose to use NOI of less than $10 million per year as the metric to decide which malls to include in the spin-off. In addition to 36.4 million square feet of mall space, Washington Prime Group also operated 16.6 million square feet of open-air power/strip centers. No other retail REIT owns a similar portfolio of assets.

Another challenge for Washington Prime Group is that the majority of its malls have Sears Holdings Corp and J C Penney Company Inc anchors, which both impact sales per square foot and present a risk factor moving forward.

However, the Washington Prime Group spin-off instantly resulted in boosting the sales per square foot metric for the remaining Simon Property Group malls from $560 to $625 -- and increased occupancy 100 basis points.

More Class-B Scale

In mid-September, Simon announced the purchase of rival Glimcher Realty Trust (NYSE: GRT), which came as surprise that few if any experts in the industry had predicted. When Simon announced the spin-off, the primary focus was said to be on the open-air centers moving forward.

When Simon spun out Washington Prime Group, it received $1 billion in cash on its balance sheet. Coincidentally, in order to fund the Glimcher acquisition, Simon is paying about $1 billion in cash for two higher end Glimcher malls located in New Jersey and Texas.

Washington Property Group gains more scale, a few west coast markets and -- most importantly -- an operational platform and management team to focus solely on improving open-air centers and Class-B asset performance moving forward.

Simon Bets On Rival Macerich Success

On November 19, shares in mall rival Macerich spiked up 9.5 percent after disclosing that 3.6 percent of its shares were now in the hands of Simon, its biggest competitor.

According to the Simon announcement, "Simon may request that Macerich waive its excess share provision, which restricts share ownership of greater than 5 percent, in light of the waiver recently granted to another investor in connection with its acquisition of a 10.9 percent share position in Macerich."

Shares of both Simon and Macerich have fared quite well since the disclosure of Simon's investment and possible increased stake in its Class-A mall competitor.

The Jury Is Still Out

While Mr. Market seems to be quite enthusiastic about the future of Class-A and A+ malls, it remains to be seen if the Simon magic can transform the Washington Prime/Glimcher combination of assets from what some currently view as a lump of coal, into a success story moving forward.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted-In: David Simon holiday shopping season OmnichannelLong Ideas REIT Trading Ideas Real Estate Best of Benzinga