Earnings Outlook For PACCAR

PACCAR (NASDAQ:PCAR) is set to give its latest quarterly earnings report on Tuesday, 2025-07-22. Here's what investors need to know before the announcement.

Analysts estimate that PACCAR will report an earnings per share (EPS) of $1.34.

Investors in PACCAR are eagerly awaiting the company's announcement, hoping for news of surpassing estimates and positive guidance for the next quarter.

It's worth noting for new investors that stock prices can be heavily influenced by future projections rather than just past performance.

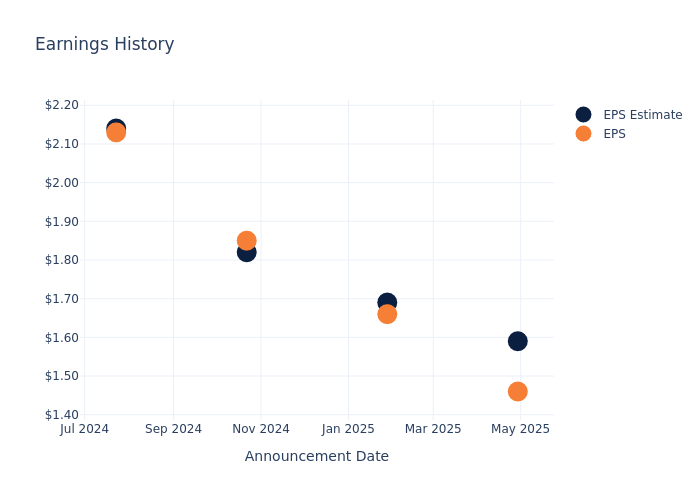

Performance in Previous Earnings

During the last quarter, the company reported an EPS missed by $0.13, leading to a 0.09% drop in the share price on the subsequent day.

Here's a look at PACCAR's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 1.59 | 1.69 | 1.82 | 2.14 |

| EPS Actual | 1.46 | 1.66 | 1.85 | 2.13 |

| Price Change % | -0.0% | 3.0% | -1.0% | 2.0% |

Tracking PACCAR's Stock Performance

Shares of PACCAR were trading at $93.68 as of July 18. Over the last 52-week period, shares are down 2.71%. Given that these returns are generally negative, long-term shareholders are likely upset going into this earnings release.

Analyst Insights on PACCAR

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding PACCAR.

PACCAR has received a total of 4 ratings from analysts, with the consensus rating as Neutral. With an average one-year price target of $100.5, the consensus suggests a potential 7.28% upside.

Analyzing Analyst Ratings Among Peers

In this analysis, we delve into the analyst ratings and average 1-year price targets of Cummins, Westinghouse Air Brake and Oshkosh, three key industry players, offering insights into their relative performance expectations and market positioning.

- Analysts currently favor an Buy trajectory for Cummins, with an average 1-year price target of $371.5, suggesting a potential 296.56% upside.

- Analysts currently favor an Buy trajectory for Westinghouse Air Brake, with an average 1-year price target of $218.67, suggesting a potential 133.42% upside.

- Analysts currently favor an Buy trajectory for Oshkosh, with an average 1-year price target of $122.64, suggesting a potential 30.91% upside.

Peer Analysis Summary

In the peer analysis summary, key metrics for Cummins, Westinghouse Air Brake and Oshkosh are highlighted, providing an understanding of their respective standings within the industry and offering insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| PACCAR | Neutral | -14.90% | $1.32B | 2.84% |

| Cummins | Buy | -2.73% | $2.15B | 7.78% |

| Westinghouse Air Brake | Buy | 4.53% | $900M | 3.15% |

| Oshkosh | Buy | -9.08% | $399.90M | 2.68% |

Key Takeaway:

PACCAR ranks at the bottom for Revenue Growth among its peers. It is in the middle for Gross Profit. PACCAR is at the top for Return on Equity.

Discovering PACCAR: A Closer Look

Paccar is a leading manufacturer of medium- and heavy-duty trucks under the premium nameplates Kenworth and Peterbilt, which are primarily sold in the Americas and Australia, and DAF, which primarily services Europe and South America. The trucks segment (74% sales) goes to market through a network of 2,200 independent dealers. Paccar maintains an internal finance subsidiary that provides retail and wholesale financing for customers and dealers (6% sales). In recent years, Paccar has aggressively grown its parts business (20% sales), which include engines, axles, and transmissions for its own truck brands as well as independent producers. The company commands approximately 30% of the Class 8 market share in North America and 15% of the heavy-duty market share in Europe.

A Deep Dive into PACCAR's Financials

Market Capitalization Analysis: Above industry benchmarks, the company's market capitalization emphasizes a noteworthy size, indicative of a strong market presence.

Revenue Growth: PACCAR's revenue growth over a period of 3 months has faced challenges. As of 31 March, 2025, the company experienced a revenue decline of approximately -14.9%. This indicates a decrease in the company's top-line earnings. When compared to others in the Industrials sector, the company faces challenges, achieving a growth rate lower than the average among peers.

Net Margin: PACCAR's net margin is below industry standards, pointing towards difficulties in achieving strong profitability. With a net margin of 6.79%, the company may encounter challenges in effective cost control.

Return on Equity (ROE): The company's ROE is below industry benchmarks, signaling potential difficulties in efficiently using equity capital. With an ROE of 2.84%, the company may need to address challenges in generating satisfactory returns for shareholders.

Return on Assets (ROA): PACCAR's ROA is below industry standards, pointing towards difficulties in efficiently utilizing assets. With an ROA of 1.17%, the company may encounter challenges in delivering satisfactory returns from its assets.

Debt Management: PACCAR's debt-to-equity ratio is below the industry average at 0.87, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for PACCAR visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.