Insights into Halliburton's Upcoming Earnings

Halliburton (NYSE:HAL) is gearing up to announce its quarterly earnings on Tuesday, 2025-07-22. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Halliburton will report an earnings per share (EPS) of $0.56.

Investors in Halliburton are eagerly awaiting the company's announcement, hoping for news of surpassing estimates and positive guidance for the next quarter.

It's worth noting for new investors that stock prices can be heavily influenced by future projections rather than just past performance.

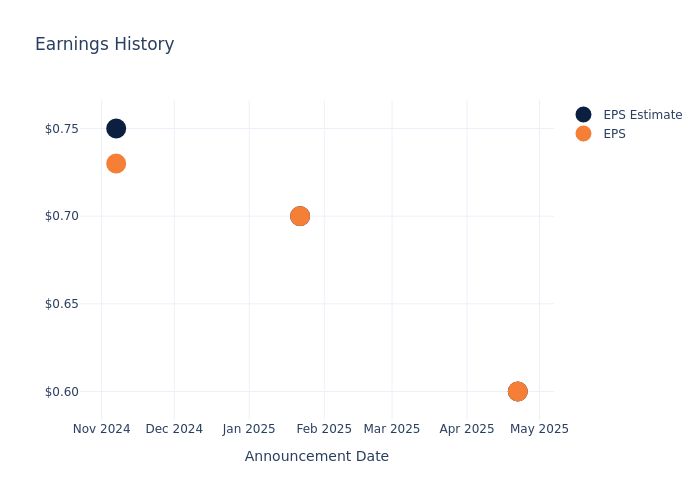

Performance in Previous Earnings

During the last quarter, the company reported an EPS missed by $0.00, leading to a 0.43% drop in the share price on the subsequent day.

Here's a look at Halliburton's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.6 | 0.7 | 0.75 | 0.8 |

| EPS Actual | 0.6 | 0.7 | 0.73 | 0.8 |

| Price Change % | -0.0% | -2.0% | -1.0% | -6.0% |

Performance of Halliburton Shares

Shares of Halliburton were trading at $21.22 as of July 18. Over the last 52-week period, shares are down 36.79%. Given that these returns are generally negative, long-term shareholders are likely a little upset going into this earnings release.

Analyst Opinions on Halliburton

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Halliburton.

The consensus rating for Halliburton is Buy, derived from 11 analyst ratings. An average one-year price target of $27.27 implies a potential 28.51% upside.

Comparing Ratings Among Industry Peers

This comparison focuses on the analyst ratings and average 1-year price targets of TechnipFMC, NOV and Weatherford International, three major players in the industry, shedding light on their relative performance expectations and market positioning.

- Analysts currently favor an Outperform trajectory for TechnipFMC, with an average 1-year price target of $40.75, suggesting a potential 92.04% upside.

- Analysts currently favor an Outperform trajectory for NOV, with an average 1-year price target of $15.44, suggesting a potential 27.24% downside.

- Analysts currently favor an Outperform trajectory for Weatherford International, with an average 1-year price target of $69.5, suggesting a potential 227.52% upside.

Summary of Peers Analysis

The peer analysis summary outlines pivotal metrics for TechnipFMC, NOV and Weatherford International, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Halliburton | Buy | -6.67% | $879M | 1.95% |

| TechnipFMC | Outperform | 9.38% | $464.90M | 4.61% |

| NOV | Outperform | -2.41% | $447M | 1.14% |

| Weatherford International | Outperform | -12.15% | $374M | 5.76% |

Key Takeaway:

Halliburton ranks at the bottom for Revenue Growth among its peers. It is in the middle for Gross Profit. For Return on Equity, Halliburton is at the bottom compared to its peers.

About Halliburton

Halliburton is North America's largest oilfield service company as measured by market share. Despite industry fragmentation, it holds a leading position in the hydraulic fracturing and completions market, which makes up nearly half of its revenue. It also holds strong positions in other service offerings like drilling and completions fluids, which leverages its expertise in material science, as well as the directional drilling market. While we consider SLB the global leader in reservoir evaluation, we think Halliburton leads in any activity from the reservoir to the wellbore. The firm's innovations have helped multiple producers lower their development costs per barrel of oil equivalent, with techniques that have been homed in over a century of operations.

Halliburton's Economic Impact: An Analysis

Market Capitalization: Positioned above industry average, the company's market capitalization underscores its superiority in size, indicative of a strong market presence.

Revenue Growth: Halliburton's revenue growth over a period of 3 months has faced challenges. As of 31 March, 2025, the company experienced a revenue decline of approximately -6.67%. This indicates a decrease in the company's top-line earnings. When compared to others in the Energy sector, the company faces challenges, achieving a growth rate lower than the average among peers.

Net Margin: Halliburton's net margin is below industry averages, indicating potential challenges in maintaining strong profitability. With a net margin of 3.77%, the company may face hurdles in effective cost management.

Return on Equity (ROE): The company's ROE is below industry benchmarks, signaling potential difficulties in efficiently using equity capital. With an ROE of 1.95%, the company may need to address challenges in generating satisfactory returns for shareholders.

Return on Assets (ROA): Halliburton's ROA lags behind industry averages, suggesting challenges in maximizing returns from its assets. With an ROA of 0.8%, the company may face hurdles in achieving optimal financial performance.

Debt Management: The company faces challenges in debt management with a debt-to-equity ratio higher than the industry average. With a ratio of 0.83, caution is advised due to increased financial risk.

To track all earnings releases for Halliburton visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.